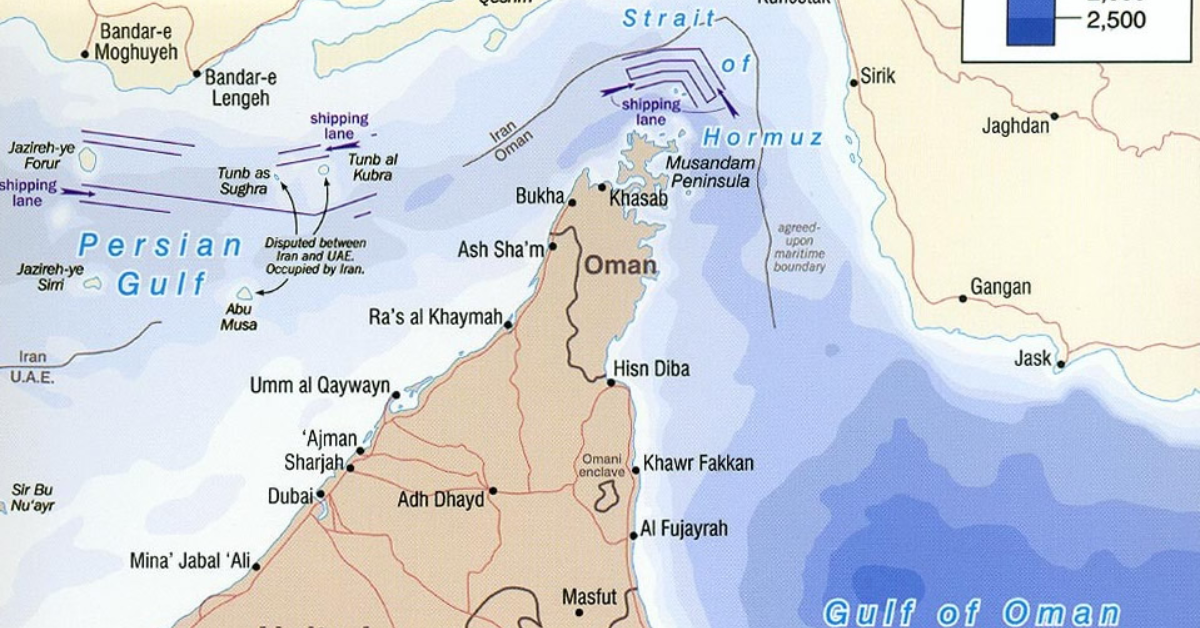

Oil prices surged approximately 2% to reach a two-week high on Monday, driven by stalled peace negotiations between the U.S. and Iran and ongoing restrictions on shipments through the Strait of Hormuz. Brent crude futures increased by $2.16, or 2.1%, reaching $107.49 per barrel, while U.S. West Texas Intermediate (WTI) saw a rise of $1.32, or 1.4%, settling at $95.72. This marks Brent’s sixth consecutive day of gains, the longest stretch since March 2025, and suggests a potential for the highest closing price since early April.

Although direct diplomatic efforts between the U.S. and Iran have paused following President Trump’s cancellation of envoy discussions, sources indicate that mediation efforts continue. Analysts emphasize that the ongoing diplomatic standoff is preventing 10 to 13 million barrels of oil from entering the international market daily, exacerbating an already tight oil supply situation. Such limitations on supply are expected to drive oil prices higher.

As inflation remains a concern, the European Central Bank’s upcoming meeting may influence interest rate decisions, especially with the ongoing geopolitical tensions. Goldman Sachs has adjusted its oil price forecasts upwards, now predicting Brent to reach $90 a barrel and WTI to hit $83, attributing these predictions to diminished output in the Middle East. Meanwhile, gasoline futures have hit their highest levels since July 2022, indicating heightened refining profit margins.

In related news, tensions have escalated in the Middle East, with the Israeli military expanding its strikes in Lebanon despite a fragile ceasefire with Hezbollah. The situation underscores the broader instability in the region, impacting both geopolitical dynamics and global oil markets.